There’s a quiet shift happening in professional services. Clients are getting better at pushing back on invoices. They want to pay for what they actually get out of an engagement, not for the number of hours your team spent in meetings or writing documentation. And that pressure isn’t going away.

Outcome-based and risk-sharing contracts are the industry’s answer to that pressure. But they’re a fundamentally different beast from time-and-materials work. The revenue model changes. The risk profile changes, too. If delivery doesn’t change with it, margins erode quietly.

This guide is about making that transition without flying blind. You’ll learn how to manage risk-sharing contracts, control scope, track KPIs, and protect margin when payment depends on outcomes, not hours.

Outcome-based contracts pay for measurable results, not effort. Payment is triggered when agreed KPIs are achieved and validated using a defined data source and time window. Clear acceptance criteria and change control protect the margin when delivery risk shifts to the provider.

Payment is released when agreed KPIs are achieved and validated against a defined data source and measurement window.

Key takeaways

- Define KPIs and validation rules before signing.

- Build milestones around outcomes, not internal tasks.

- Treat scope changes as financial events.

- Track margin weekly to catch drift early.

- Use binary acceptance criteria to avoid “90 percent done.”

Why outcome-based contracts are rising

More service firms are hearing the same question from clients:

“If the goal is measurable business impact, why are we paying for hours?”

Clients are not challenging capability. They are challenging the logic of time-based pricing in a results-driven environment. Several forces are pushing outcome-based contracts to the forefront.

1. Clients want pricing tied to measurable impact

Procurement teams are under pressure, and executive sponsors want visible ROI. When success is defined in terms of adoption, revenue growth, or performance improvement, hourly billing can feel disconnected from value. Outcome-based contracts align payment with results rather than effort.

2. Margin pressure is increasing for service firms

Professional services firms are facing rising salary costs and tighter labor markets. Utilization alone is no longer a dependable buffer. Outcome-based or risk-sharing models offer a way to differentiate and potentially protect margin through stronger value alignment.

3. Competitive differentiation matters more

In crowded markets, confidence becomes a selling point. Offering outcome-based pricing signals belief in your delivery capability. It positions the firm as accountable for impact, not just activity.

4. Incentives are better aligned

When compensation depends on performance benchmarks or adoption rates, both parties focus on outcomes rather than hours consumed. This alignment can strengthen partnership dynamics, but it also increases delivery accountability.

5. Risk shifts toward the service provider

Payment may depend on variables such as performance targets or revenue impact. That means delivery discipline must increase. If projects are still managed as if effort equals value, financial exposure becomes visible quickly.

When outcome-based makes sense

Outcome-based contracts are not automatically better than time and materials. They work well in the right conditions and create unnecessary friction in the wrong ones. Before committing to a risk-sharing model, it helps to step back and assess whether the environment supports measurable delivery.

In general, outcome-based pricing makes sense when the variables influencing success are reasonably understood and both sides are willing to share responsibility for the result.

It tends to work best when:

- Outcomes are measurable with shared data access

- The client can commit to owners, training, and fast decisions

- Success criteria can be written in objective terms

- The work has repeatable patterns and predictable drivers

When to avoid it

There are also situations where outcome-based contracts create more risk than value. The problem is not the pricing model itself, but the level of uncertainty surrounding the outcome.

If too many critical factors sit outside your influence, you may end up carrying risk you cannot realistically manage.

Be cautious when:

- Outcomes depend on too many uncontrolled variables.

- Data is inconsistent, delayed, or “politically owned.”

- Scope is likely to change every week.

- The client cannot commit time, approvals, or change support.

What changes when payment is tied to results

When payment depends on outcomes, the definition of progress shifts. Completing tasks is no longer enough. Delivering measurable impact becomes the standard.

On a traditional project, progress can be shown through phases completed or tasks checked off. On an outcome-based contract, the client is focused on whether the agreed metric moved. That shift affects planning, communication, risk exposure, and even revenue recognition.

Several structural changes follow.

Progress is measured by impact, not activity

In time-based models, finishing phase two signals advancement. In outcome-based models, finishing phase two means little unless it contributes to a measurable result.

This forces teams to:

- Plan around impact milestones rather than internal phases

- Communicate progress in terms of business results

- Align reporting with agreed performance indicators

If progress is still framed around effort instead of impact, misalignment appears quickly.

Risk exposure increases

Under traditional billing, overruns can often be absorbed or rebilled. Under outcome-based pricing, excess effort becomes your cost.

- If the estimates are wrong, the margin absorbs the difference

- If the scope expands informally, profitability erodes quietly

- If performance targets are not met, payment may be delayed or reduced

You cannot recover margin simply by logging more hours. Payment is contingent on results.

Revenue recognition becomes more complex

Traditional delivery models often allow revenue to be recognized as work is completed. Outcome-based contracts may require measurable proof before revenue can be recognized.

This creates a risk:

Delivery may feel nearly complete, but revenue cannot be booked because performance evidence is not yet validated.

Projects can drift into a “near-finished” state where:

- Effort continues

- Costs accumulate

- Payment waits

Without structure, that gap becomes financially dangerous.

Traditional delivery models struggle

Many firms attempt to manage outcome-based contracts using time-and-materials structures:

- Detailed task plans

- Hours logged and reviewed

- Utilization monitored

On the surface, everything appears disciplined. But those controls are built for effort management, not impact management.

If milestones are defined as internal work phases rather than contractual performance commitments, they lose commercial meaning. If KPI definitions are vague or aspirational, acceptance becomes subjective. If scope adjustments happen informally, margin erodes without visibility.

Over time, the tension builds. Delivery looks complete internally. Financial recognition lags externally.

Practical guide: running outcome-based delivery with discipline

Outcome-based contracts demand more than commercial confidence. They require structural discipline. When payment is tied to results, ambiguity becomes expensive. The following steps create the operational clarity needed to protect both margin and credibility.

Step 1: Define measurable KPIs before signing

Success must be defined before the contract is signed, not during delivery.

Start by translating strategic goals into precise metrics. If the client wants efficiency, quantify it. That might mean reducing processing time by 20 percent or eliminating a defined number of manual hours per week. If the goal is growth, define the revenue increase or conversion uplift in measurable terms.

Equally important is defining how success will be validated. Identify the data source, the measurement period, and the approval authority. Clarify what evidence is considered authoritative and under what conditions the KPI is deemed achieved. Ambiguity during negotiation feels harmless. During delivery, it becomes costly.

KPI definition checklist

- Baseline: starting point, with a date.

- Measurement window: when results are counted.

- Source of truth: dashboard, system, or report used to validate.

- Owner: who calculates and who signs off.

- Auditability: can both sides verify the same numbers.

- Controllability: what you influence vs what depends on the client.

📚 Read more: Key project financial KPIs every services firm should track

Step 2: Build milestones around outcomes, not tasks

Outcome-based engagements should be structured around commercially meaningful checkpoints.

Each milestone should represent a measurable step toward the agreed result, not just internal effort. Avoid labels like “configuration complete.” Instead, define impact-based milestones such as “system live with performance benchmark validated.” That distinction keeps delivery aligned with commercial reality.

Internally, implement a review process before presenting deliverables for validation. This protects credibility and reduces rework.

Example: In Birdview, milestone checkpoints can be tied to defined outcome criteria, with dashboards showing which outcomes are achieved, pending validation, or at risk. This shifts portfolio conversations from time spent to impact delivered.

Step 3: Treat scope changes as financial events

In outcome-based contracts, scope adjustments alter risk and margin assumptions. They are not minor operational tweaks.

Every change request should be formally documented and assessed for its impact on effort, timelines, and KPI probability. Informal collaboration may feel efficient, but it often weakens commercial clarity. Recalculate forecasts and adjust terms when necessary.

Example: Birdview allows scope changes to be recorded within the project record, with budgets and expected revenue updated accordingly. This creates an audit trail and keeps financial projections aligned with delivery conditions.

Step 4: Monitor risk and margin continuously

Risk-sharing contracts require active oversight.

Maintain a living risk register that separates technical feasibility from commercial exposure. Review it regularly and pair it with financial tracking. Compare planned versus actual effort, monitor cost accumulation, and watch for early signs of margin compression.

Waiting for quarterly reviews invites financial drift.

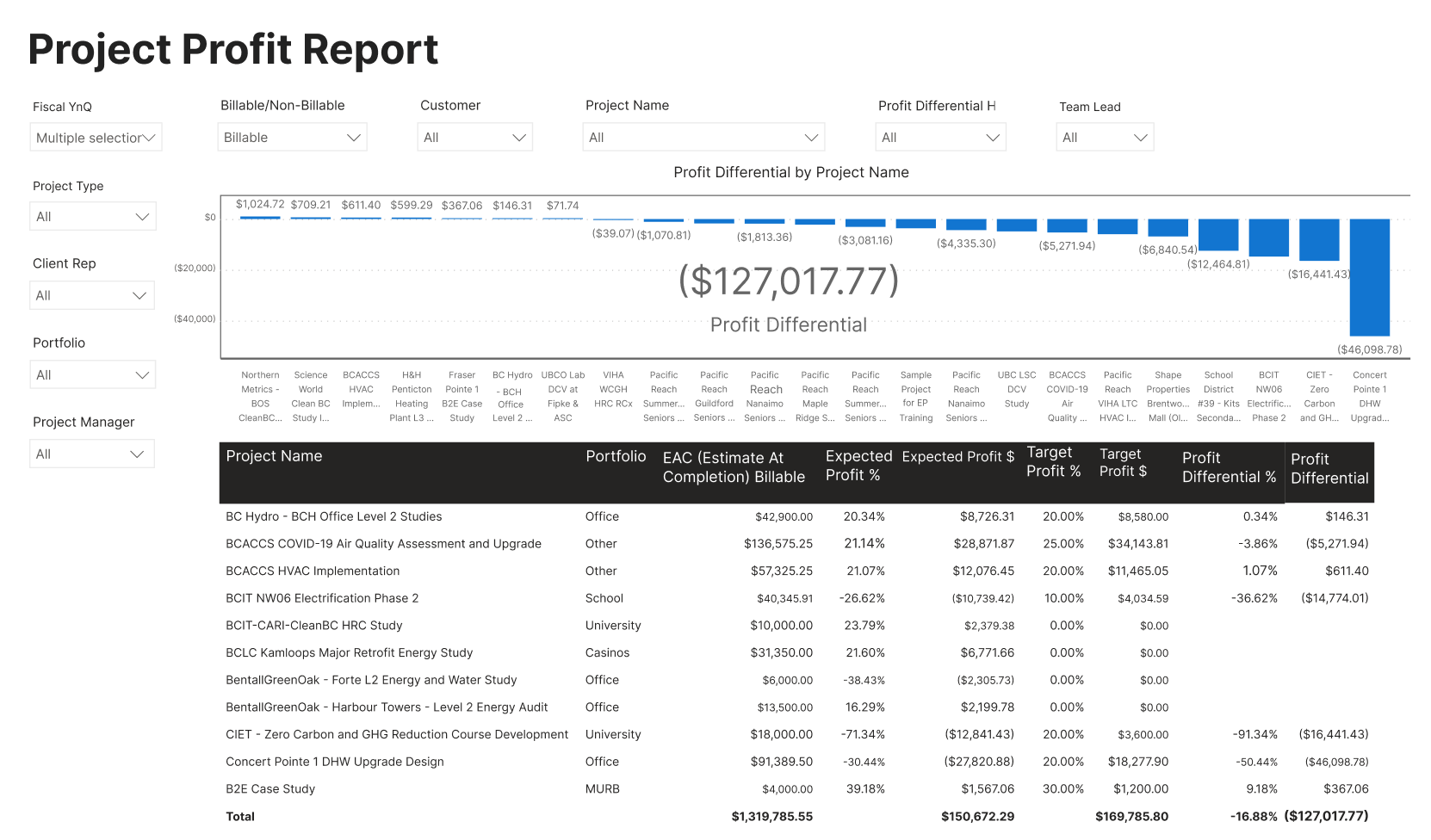

Example: Birdview‘s project profit reports provide real-time visibility into margin trends. When combined with workload and capacity views, they highlight strain or over-allocation that could threaten delivery performance.

Step 5: Eliminate the “90 percent done” syndrome

The “almost finished” problem usually stems from vague acceptance criteria.

Define completion in binary terms. A milestone is either achieved or it is not, based on predefined evidence. Require formal validation before progressing. If validation stalls, track it visibly and address it deliberately.

How Birdview helps you stay in control of financial performance

Outcome-based contracts do not fail because teams work too little. They fail because financial drift goes unnoticed for too long.

When payment is tied to milestones or measurable outcomes, revenue does not rise steadily with effort. Costs accumulate daily. Revenue may only move when a milestone is formally accepted. That gap creates exposure. If you only assess profitability at the end of the project, you are not managing risk. You are simply discovering it.

To stay in control, you need real-time visibility.

See effort versus recognized revenue at any moment

At any point during delivery, you should be able to answer three questions clearly:

- How much effort have we spent so far?

- How much revenue have we recognized based on achieved milestones?

- Are we tracking according to the financial assumptions we made at the start?

Birdview‘s project profit reports bring these numbers together in one place. Because time tracking connects directly to cost rates, and revenue can be linked to milestone completion, you are looking at real financial exposure, not disconnected data.

If costs are rising faster than revenue recognition, you will see the imbalance early. That early visibility gives you room to act.

Detect margin drift before it becomes a write-off

Financial drift rarely appears overnight. It starts subtly. A milestone takes longer than planned. A specialist spends more hours than expected. A small scope addition slips in without commercial adjustment.

Individually, these shifts seem manageable. Combined, they compress the margin.

Birdview allows you to compare planned versus actual cost and revenue progression throughout delivery. You can review margin trends at the project level and roll them up across your portfolio. If one engagement starts to deviate from its expected ratio of effort to revenue, you do not have to wait until quarter-end to notice.

That timing matters. Early detection creates options.

You may decide to tighten the scope. You may renegotiate milestone sequencing. You may reassign resources to improve efficiency. Those decisions are only available when the data is visible while the project is still in motion.

Forecast forward, not backward

Looking at current performance is important. Projecting forward is even more critical in risk-sharing models.

If current trends continue, what will the final margin look like? Will the remaining work generate more value than it costs to deliver?

Birdview‘s financial views help you forecast based on actual performance to date. Instead of reacting to past numbers, you can evaluate likely outcomes and adjust before financial damage compounds.

This forward-looking visibility is often what separates disciplined firms from reactive ones.

The core shift: from tracking hours to managing outcomes

Outcome-based contracts are hard to run well. They require clear KPIs, tight scope control, and financial visibility throughout delivery.

Tools matter less than habits. But having milestones, budgets, time tracking, and risk signals in one place makes discipline easier to maintain. Birdview is built for that visibility. It helps you catch margin drift early and keep delivery tied to the outcomes your clients pay for.

FAQ

Q: What’s the difference between outcome-based and risk-sharing contracts?

A: Outcome-based contracts tie payment directly to results. Risk-sharing contracts go a step further and distribute the financial upside or downside between vendor and client based on performance. In practice, many agreements blend both approaches.

Q: How do you handle KPIs that are outside your direct control?

A: This is one of the trickiest aspects of outcome-based work. The best approach is to define leading indicators that you can influence, alongside the lagging outcome metrics. That way, you can demonstrate progress even before the final result is measurable. Agree on this framework upfront so there are no surprises.

Q: What happens when a client changes requirements mid-delivery?

A: Treat it as a formal scope change and assess the impact on your delivery plan and the risk-sharing arrangement before agreeing to it. The conversation is easier to have before the work is done than after.

Q: How often should you review the margin on outcome-based work?

A: Weekly at minimum, ideally with a real-time dashboard, you can check between reviews. Margin erosion on outcome-based contracts tends to happen gradually, and catching it early is the only way to respond effectively.

Further reading: